JIL Information Technology Ltd. Vs ACIT (ITAT Lucknow)

Conclusion: Where payment made to foreign entities by way of retainership fee did not result in commensurate business in USA in the year relevant to assessment year 2008-09, it did not imply that the expenditure incurred was not for the purpose of the assessee’s business. AO was directed to delete the addition of Rs.64,88,451/- by observing that the expenditure was disallowed u/s 14A.

Held: Assessee-company was a computer software company. During the year under consideration it entered into an agreement with two foreign agents M/s ASP Services LLC and M/s Tekorigin LLC. Assessee had debited its profit & loss account by Rs.64,88,451/- on account o f payments being made to these foreign agents. AO while framing the assessment order against assessee disallowed the expenses of Rs.64,88,451/- by observing that the expenditure of Rs.64,88,451/- was disallowed u/s 14A. It was held that mere fact that the payment made to the aforesaid entities by way of retainership fee did not result in commensurate business in USA in the year relevant to assessment year 2008-09 did not imply that the expenditure incurred was not for the purpose of the assessee’s business. Considering that the retainer ships were terminated by the assessee within a short time when the assessee realized that the services provided by the aforesaid entities were not satisfactory. There was no requirement in law that every expenditure incurred by the assessee must result in profit. It was sufficient if the expenditure not being in the nature of capital expenditure or personal expenses was laid out or expended wholly and exclusively for the purposes of business. AO was directed to delete the aforesaid addition of Rs.64,88,451/-.

FULL TEXT OF THE ORDER OF ITAT LUCKNOW

(A) This appeal has been filed by the assessee for assessment year 200809 against impugned appellate order dated 25/03/2014 passed by learned Commissioner of Income Tax (Appeals) [“CIT(A)” for short]. The original grounds of appeal were subsequently revised by the appellant assessee. The revised grounds of appeal are as under:

“Revised Ground No. 1 & 2 (Addition of Rs.64,88,451/-)

(i) Appellant in the present case is a computer software company. During the year under consideration it entered into an agreement with two foreign agents M/s ASP Services LLC and M/s Tekorigin LLC. Copies of agreements are placed at pages 65-68 and 69-72 of the paper book.

(ii) During the year under consideration, appellant has debited its profit & loss account by Rs.64,88,451/- on account o f payments being made to these foreign agents. Total income earned for the year under consideration from the export o f the software has been at Rs.9,73,599/-. Payments to these agents were made after deduction of tax thereon and this is not in dispute. Out of total expenses of Rs.64,88,451/-debited to the Profit and Loss Account, amount to the extent of Rs.14,39,631/- was provisional entry, which was reversed on 31.10.2010 and taken to the income in A. Y. 2011-2012.

Copy of ledger account of Rs.64,88,451/- along with the bills raised by the appellant is placed at pages 73 to 82 of the paper book.

(iii) The Ld. A.O. while framing the assessment order against the appellant disallowed the expenses of Rs.64,88,451/- by observing that

(a)The expenditure of Rs.64,88,451/- is disallowed u/s 14A of the I.T. Act.

(b) Income from “export of software “is only Rs.9,73,599/-against which expenditure of Rs.64,88,451/- is quite irrational and unjustified.

(c) The genuineness of the expenditure could not be proved by the assessee and

(iv) Before moving to comment on the observations made by the Ld. A.O. it is pertinent to mention that during the whole o f the assessment proceedings, the Assessing Authority never confronted the assessee with any sort of queries as to establish the genuineness of the expenditure o f Rs.64,88,451/- but while framing the assessment order, he made the addition by alleging that genuineness of the expenditure of Rs.64,88,451/- was not established by the assessee.

With a view to assist your honours, following documents have been placed in the paper book to establish that no query was raised:

(a) Copy of questionnaire dated 10.08.2010 is placed at pages 145 to 146 of the Paper Book.

(b) Copy of assessee’s reply dated 02.09.2010 is placed at pages 147 to 148 of the paper book.

(c) Copy of assessee’s reply dated 16.09.2010 is placed at pages 149 of the paper book.

(d) (d) Copy of order sheet entry is placed at pages 150 o f the paper book.

Reliance is placed on the case authorities Chartered Accountants of India Vs. L. K. Ratna 1987(164)-ITR-0001 (SC) placed at pages 244 to 259 of the paper book and also Maneka Gandhi Vs. Union of India (1981)-1SCC 644 at page 709 para 94, placed at page 260 of the paper book.

In both these cases, it has been held that violation o f principal of natural justice cannot be cured by the appellate authority.

(v) In the present case, specific ground was taken before the Ld. CIT(A) regarding the applicability of section 14A of the Act but the Ld. CIT(A) did not appreciate the facts and the merit of the case and he confirmed the addition. All the supporting documents were also furnished. Regarding the observations made by the Ld. A.O, our brief submissions are as under-

(A) Regarding applicability of section 14A of the Act:

As the appellant has not claimed any income as exempt against the expenses debited to the profit & loss Account, there is no scope of any disallowance u/s 14A of the Act and on this ground also addition of Rs.64,88,451/- deserves to be deleted. No applicability of Section 14A when no income is claimed as exempt as held in M/s Redington (I) Ltd. in 392 ITR 633) Copy of Balance Sheet and Profit & Loss Account for the F.Y. 2007-2008 is placed at pages 1 to 23 of the Paper Book. (Relevant page 6)

Copy of acknowledgement of return and computation o f income is placed at pages 238 to 243 (Relevant page 238 & 239)

(B)Regarding genuineness of the expenditure:

Before the Ld. CIT(A) all the evidences containing more than 300 pages were filed to establish the genuineness of the expenses. The same was sent for the remand report. Ld. A.O. submitted his remand report and at no point of time, the documents / evidences submitted by the appellant were disputed. Even in remand report, the A.O. was insistent on the applicability of section 14A of the Act. The CIT(A) did neither appreciate the facts of the case nor legal aspects o f the case and confirmed the addition.

Moreover, with a view to assist the Hon’ble Bench, following papers are placed in paper book.

(i) Copies of correspondences made with the foreign agents are placed at pages 178 to 235 of the paper book.

(ii) Copy of bills/ invoices raised to foreign agents are placed at pages 167 to 177 of the paper book.

(iii) Copy of work order is placed at pages 236 to 237 of the paper book.

(iv) Copies of TDS certificates issued to LLC are placed at pages 156 to 158 of the paper book.

(v) Copies of request letters to bank for clearing remittances to LLC are placed at pages 159 to 162 of the paper book.

(vi) Copies of CA certificates are placed at pages 163 to 166 of the paper book.

(vii) Copies of confirmation letters obtained from these LLs are placed at pages 154 to 155 of the paper book.

(viii) Copy of remand report of the A.O. is placed at pages 86 to 87 of the paper book.

(ix) Copy of rejoinder on remand report is placed at pages 92 to 94 of the paper book.

The Ld. CIT(A) in his order sheet entry itself has recorded the satisfaction of the evidences being provided by the appellant towards the genuineness of the expenditure. Order sheet entry is as under-

“Shri S.K.Bhardwaj, AR of the appellant attended with Shr i Gajendra Singh head of the finance of the appellant company. He has furnished the details of services rendered by ASP Services LLC and Tekorigin LLC Copy of order sheet entry is placed at pages 151 to 153 of the paper book. (Relevant page is 153)

(C) Regarding Income from “export of software” is only Rs.9,73,599/-against which expenditure of Rs.64,88,451/- is quite irrational and unjustified,

During the year under consideration appellant has earned income of Rs. 9,73,599/- from export of software against expenditure of Rs.64,88,451/-. Details of revenue and expenditure for three years are placed at page119 of the paper book.

(D) Regarding violation of principal of natural justice:

The Ld. CIT(A) in his appellate order has quoted a number o f case authorities. But in all these case authorities, queries were raised by the Assessing Authority and assessee failed to make compliance. In the present case, no sort of query was raised. So none of the case authorities quoted by the Ld. CIT(A) is applicable in the present case.

Assessment order is liable to be quashed on the ground o f violation of natural justice also.

(vi) Reliance is placed on the following case authorities: 1. On Genuineness of expenses :

(a) Eastern Investments Ltd Vs. CIT 1951-(020)-ITR 0001-SC (Page 261-267 of the paper book)

(b) CIT Vs. Delhi Safe deposits Co. Ltd of the paper book) 1982-133-ITR 756-SC (Page 268 to 273

(c) DCIT Vs. Vodafone Mobile Services Ltd 2016-(130)-DTR-195 (ITAT Delhi) (pages)

(d) Additional CIT Vs. Rajasthan Spinning and weaving Mills Limited (2005)-274-ITR – (Pages 135 to 144 of the paper book.)

(e) CIT Vs. Modern Insulators Ltd. [2014-110 DTR 297 (Raj) ]

(f) CIT Vs. Atma Prakash Batra [ 2012- (340)-ITR 0177-Guj ]

(g) DCIT Vs. M/s Super Tannery (India) Ltd [2004 (4) MTC 838 (All)

(h) CIT vs. Mouan Export India (P) Ltd. 162 DTC 247 (Del)

2. No disallowances of expenses when TDS was deducted and deposited

(a) ITO Vs. LGW Ltd 2016-(130)-ITR 201 (ITAT KOL) (Pages 280-298 of the paper book)

3. It is not required that expenditure must necessarily relate to earning of income.

(a) Brihan Maharastra Sugar Syndicate Ltd and others Vs. DCIT 165 R 279 (Bom) (pages 299 to 313 of the paper bok)

2. Revised Ground No. 3

Ld. CIT(A) has not allowed the credit of TDS of Rs.92,20,398/-Copy of acknowledgement of return along with computation o f income showing credit of TDS is placed at pages 238 to 243 o f the paper book. ”

(A.1) Although several grounds of appeal have been raised by the assessee, in effect there are only two issues in dispute. The first issue is regarding the addition of Rs.64,88,451/- made by the Assessing Officer u/s 14A of the I. T. Act. The second issue in dispute is regarding the assessee’s claim for TDS.

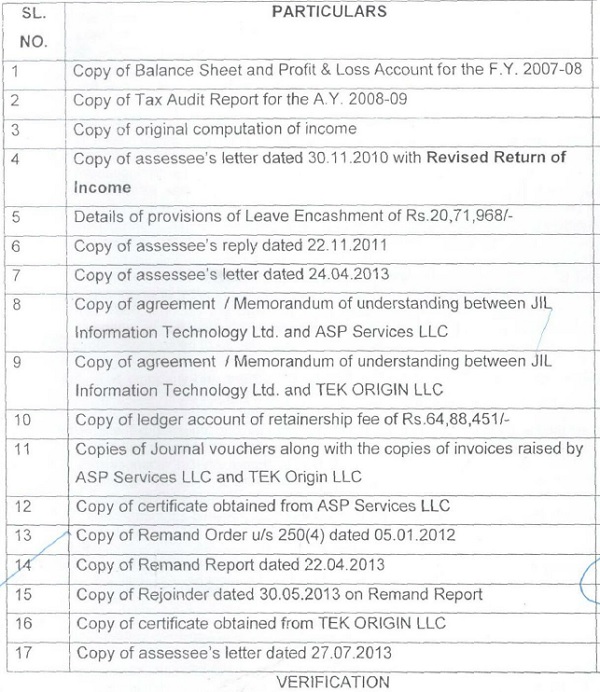

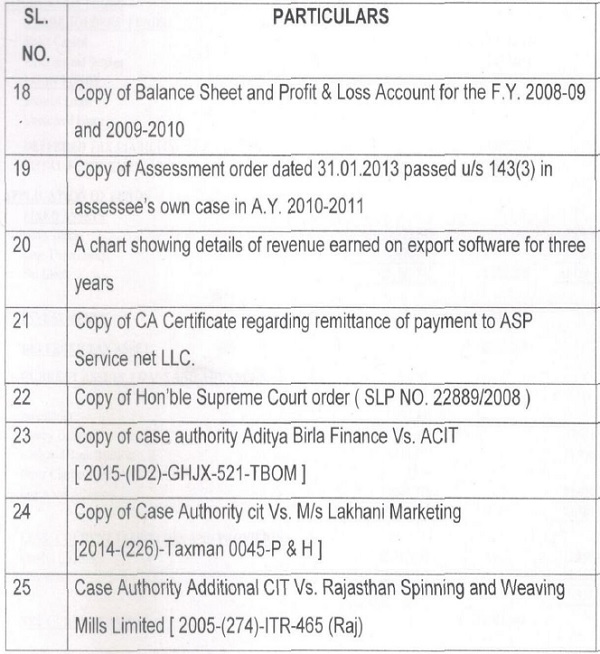

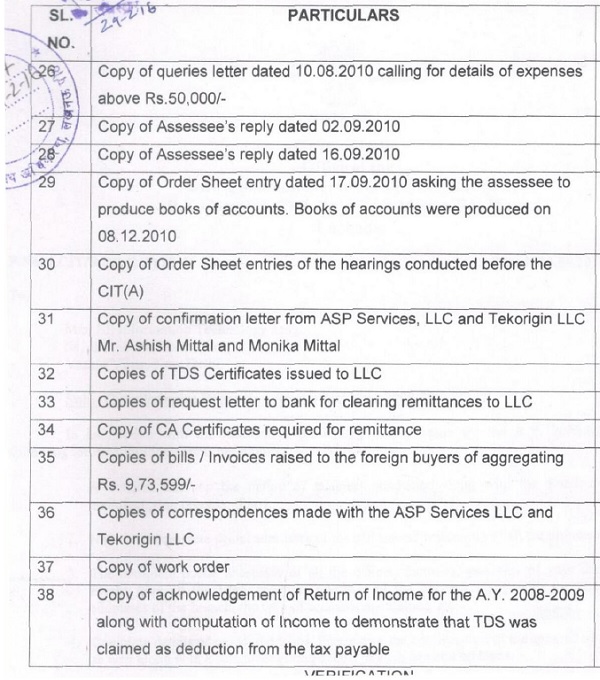

(A.2) In the course of appellate proceedings before the Income Tax Appellate Tribunal, the paper books, containing the following particulars were filed from the assessee’s side:

(B) As regards the addition of Rs.64,88,451/- made by the Assessing Officer under section 14A of the Act, the learned A.R. for the assessee submitted that there was no exempt income in the hands of the assessee and therefore, there was no case for any disallowance u/s 14A of the Act. As regards the genuineness of the aforesaid expenditure of Rs.64,88,451/-, he contended that there was no dispute. In this context, he highlighted that tax was deducted at source from payments made by the assessee by way of retainership fees. As regards whether the expenditure was incurred for the purposes of the assessee’s business, he drew our attention to the various documents contained in the paper book. He explained that the aforesaid amount of Rs.64,88,451/- was paid by the assessee to ASP Services LLC (“ASP” for short” and M/s Tekorigin LLC (“TEK for short”) both entities based in USA, as retainership fees for marketing of the assessee’s software in USA as well as for business development in USA. He drew our attention to copies of agreements of the aforesaid entities namely ASP and TEK respectively. He also drew our attention to copies of journal vouchers along with copies of invoices raised by the aforesaid entities. He further drew our attention to copy of ledger account of retainership fee. He also drew our attention to the fact that the retainership with the aforesaid two entities, though subsequently terminated, resulted in substantial amount of business for the assessee in the year under consideration and in subsequent years. He further drew our attention to correspondence of the assessee (including through e-mail) with the aforesaid ASP and TEK. Based on the aforesaid submissions, the learned A.R. for the assessee contended that the aforesaid addition of Rs.64,88,451/- should be deleted.

(B.1) Learned D.R. for Revenue opposed this contention of the learned A.R. for the assessee. He highlighted the fact that the business secured by the assessee in USA during the year under consideration was not commensurate with the payment made to the aforesaid two entities by way of retainership. Therefore, he submitted that the payment made to the aforesaid two entities do not deserve to be deleted.

(B.2) In his rejoinder, the learned A.R. for the assessee conceded that the business secured during the year in USA, as a result of aforesaid retainership, was not satisfactory. Therefore, he submitted, theretainerships were terminated within a few months because the assessee was not satisfied with the services of the aforesaid entities, namely ASP and TEK. However, he once again highlighted that the efforts made by the aforesaid entities resulted in good business in subsequent years. He further contended that the mere fact that the payments made did not result in expected benefits, cannot lead to the conclusion that the payment made was not for the purpose of business.

(C) We have heard both the sides. We have perused the materials on record. It is not in dispute that the assessee did not have any exempt income during year. Therefore, we categorically hold that any disallowance u/s 14A was unwarranted in this case. Further we find that the genuineness of the aforesaid expenditure is not in dispute. Further it is also found that the aforesaid entities namely ASP Services LLC and M/s Tekorigin LLC did provide services to the assessee. The services provided by the aforesaid entities to the assessee are evidenced by copies of correspondences forming part of the paper book as well as on the other documents referred to in the foregoing paragraphs (B) of this order. It is also not in dispute that the assessee got good business in USA in subsequent years. In view of the foregoing, we agree with the contention of learned A.R. for the assessee that the mere fact that the payment made to the aforesaid entities by way of retainership fee did not result in commensurate business in USA in the year relevant to assessment year 2008-09 does not imply that the expenditure incurred was not for the purpose of the assessee’s business. We are further persuaded to take this view considering that the retainer ships were terminated by the assessee within a short time when the assessee realized that the services provided by the aforesaid entities were not satisfactory. There is no requirement in law that every expenditure incurred by the assessee must result in profit. It is sufficient if the expenditure not being in the nature of capital expenditure or personal expenses is laid out or expended wholly and exclusively for the purposes of business. In view of the foregoing, we direct the Assessing Officer to delete the aforesaid addition of Rs.64,88,451/-.

(D) The second dispute is regarding credit for TDS. In this regard the learned A.R. for the assessee submitted that the Assessing Officer be directed to give credit for TDS in accordance with law. Learned D.R. for Revenue expressed no objection to this. Accordingly, we direct the Assessing Officer to give credit to the assessee for tax deducted at source in accordance with law.

In the result, the appeal of the assessee is partly allowed.

(Order pronounced in the open court on 21/01/2025)