Daljeet Singh Gill Vs Union of India & Ors. (Delhi High Court)

Delhi High Court ruled that the absence of proof of service of notice cannot be a ground to presume a pending investigation and disqualify a taxpayer under the Sabka Vishwas (Legacy Dispute Resolution) Scheme, 2019. The case involved Daljeet Singh Gill, who sought relief under the Scheme for unpaid service tax liabilities for FY 2015-16 and 2016-17. However, his application was rejected without explanation. A subsequent show cause notice issued on December 31, 2020, alleged a tax liability of Rs. 11,26,937 along with penalties. The petitioner challenged the rejection and the show cause notice, arguing that no valid basis for disqualification was provided.

During the proceedings, the tax authorities relied on notices dated October 2019 and clauses 125(1)(e) and 125(1)(f) of the Scheme, which bar applicants under certain conditions, including pending investigations. However, the court found that there was no conclusive proof of service of the October 2019 notice. The department admitted that it lacked original dispatch records or evidence that the petitioner was notified in time. In the absence of such proof, the court held that the petitioner could not be disqualified under the Scheme, as an investigation must be demonstrably pending at the time of application.

The court also referred to a CBIC circular dated September 25, 2019, clarifying that merely calling for financial documents does not automatically constitute an “investigation” under the Scheme. Judicial precedents affirm that taxpayers should not be denied benefits arbitrarily. Courts have consistently ruled that procedural lapses by tax authorities cannot be used to penalize taxpayers, emphasizing the need for due process and proper notice. The Delhi High Court followed similar reasoning, emphasizing that disqualification must be supported by clear evidence.

Since the Scheme was no longer operational, the court directed the tax authorities to accept the petitioner’s declaration of Rs. 11,26,937, provided he deposits the amount within a month. If the payment is not made within the stipulated time, the show cause notice would revive, allowing the petitioner to respond per legal procedures. This ruling reinforces the importance of procedural fairness in tax disputes and prevents arbitrary disqualification from tax amnesty schemes.

FULL TEXT OF THE JUDGMENT/ORDER OF DELHI HIGH COURT

1. This hearing has been done through hybrid mode.

2. The present petition has been filed under Articles 226 and 227 of the Constitution of India, inter alia, challenging the Show Cause Notice dated 31st December, 2020 passed by the Deputy Commissioner, Central Tax, Goods and Services Tax, Gurugram.

3. It is the case of the Petitioner-Daljeet Singh Gill that he is running a business under the name and style of M/s Dhartiputra Infotech Inc., which provides Consultation (Business Auxilliary Services). The Petitioner is stated to have failed to deposit the service tax pertaining to the Financial Year 20152016 and 2016-2017 w.e.f. 1st April, 2017 to 30th June, 2017.

4. To remedy this situation, the Petitioner applied for resolution of his past disputes as a one time measure under the Sabka Vishwas (Legacy Dispute Resolution) Scheme, 2019 (hereinafter “the Scheme”). However, as per the Petitioner the Respondents have rejected the Petitioner’s plea to resolve its disputes without providing any reason. Hence, the present petition.

5. On 30th December, 2019 the Petitioner applied to avail the benefit of the Scheme via Application Reference No. LD3012190011883, and declared the tax liability of Rs.11,26,937/-. According to the Petitioner, the said application was rejected on 8th January, 2020 vide an email from the Respondents. The said e-mail received by the Petitioner reads as under:

“Dear taxpayer, your SVLDRS Form for the ARN No.LS3012190011883 has been rejected”

6. The Petitioner again applied on 15th January, 2020, however, the second time also the application under the Scheme was rejected on 27th January, 2020.

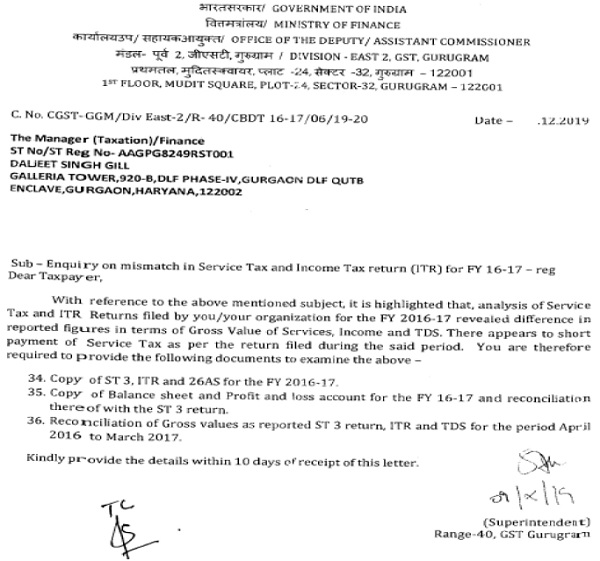

7. It is stated that an employee of the Petitioner visited the office of the Respondent sometime in January, 2020. He was handed over a copy of notice bearing No. CGST-GGM/Div East-2/R-40/ CBDT 16-17/06/19-20. The said notice was stated to have been signed on 09th October, 2019, however, the date mentioned in the notice was “…12.2019”. The said notice is extracted hereunder for reference:

8. Again on 15th September, 2020 the Petitioner received an e-mail from the Respondents with three documents attached thereto, which showed that certain queries have been raised in respect of the Petitioner’s company’s Service Tax Account.

9. According to the Petitioner, the impugned show cause notice was then issued on 31st December, 2020 claiming that the Petitioner was liable to pay service tax of Rs.11,26,937/- along with penalty. A reply was sent by the Petitioner, however, under the said show cause notice proceedings is stated to be pending.

10. A perusal of the counter-affidavit would show that the department relies upon the said three notices as also Clause 125(1)(e) and 125(1)(f) of the Scheme to disqualify the Petitioner under the Scheme. The said notices as also the email communication have been perused by the Court. Clearly, these notices do not appear to have been part of the initial email rejecting the application of the Petitioner.

11. On 10th December, 2024, after having perused the counter affidavit, since there was a doubt as to whether the notices under Clauses 125(1)(e) and 125(1)(f) of the Scheme under which the Petitioner was disqualified, were sent to the Petitioner or not, the Court had directed as under:

“11. Accordingly, it is directed as under:

a. The Petitioner shall produce the original copy of both the e-mails in order to confirm that there was no attachment to the said e-mails. The Department shall also produce the emails to show if there was any attachment.

b. The Department shall also produce any proof of service of these notices at pages 11 to 14 with the counter-affidavit and the date when the said notices were served upon the Petitioner.”

12. Pursuant to the above order, certain printouts from Yahoo mail were filed by the Petitioner. However, no document was filed by the Department. Accordingly, upon request, on 27th January, 2025 one more opportunity was again given.

13. Mr. Tripathi, ld. Sr. Standing Counsel today submits that a short affidavit has been filed yesterday i.e., 19th February, 2025. The same is, however, not on record. A hard copy has been handed across to the Court, as per which, again, it becomes clear that the October, 2019 notice which has a dispatch date of 7th October, 2019, has no proof of service.

14. Mr. Tripathi, ld. Sr. Standing Counsel for the Department further submits that though there may be a dispatch register, the original would not be available and there is no proof available with the Department, as on date, of dispatch of the letter or service upon the Petitioner.

15. When such is the position, the Petitioner’s disqualification under the Scheme would not arise inasmuch as under Clauses 125(1)(e) and 125(1)(f) of the Scheme, unless and until there was a pending investigation, the Petitioner could not have been disqualified under the same. The said clauses are extracted hereunder:

“125. (1) All persons shall be eligible to make a declaration under this Scheme except the following, namely:— […]

e. who have been subjected to an enquiry or investigation or audit and the amount of duty involved in the said enquiry or investigation or audit has not been quantified on or before the 30th day of June, 2019;

f. a person making a voluntary disclosure,—

i. after being subjected to any enquiry or investigation or audit; or

ii. having filed a return under the indirect tax enactment, wherein he has indicated an amount of duty as payable, but has not paid it;”

16. Further, the import of Clause 125(1)(f) has been clarified by the Central Board of Indirect Taxes and Customs (hereinafter “CBIC”) vide Circular dated 25th September, 2019 reads as under:

“(vi) Section 125(1)(f) bars a person from making voluntary disclosure after being subjected to an enquiry or investigation or audit. Further, what constitutes an enquiry or investigation or audit has also been defined [Sections 121(g) and 121(m)]. A doubt has been expressed as to whether benefit of the Scheme would be available in cases where documents like balance sheet, profit and loss account etc. are calledfor by department, while quoting authority of Section 14 of the Central Excise Act, 1944 etc. It is clarified that the Designated Committee concerned may take a view on merit, taking into account the facts and circumstances of each case as to whether the provisions of Section 125(1)(f) are attracted in such cases.”

17. Since there is no proof on record that there was any investigation on the date when the Petitioner applied to avail the benefit under the Scheme and the fact that the orders disqualifying the Petitioner which have been passed are also completely unreasoned and one-line orders, this Court is of the opinion that the Petitioner is entitled to relief. However, the scheme is no longer operational. Under these circumstances, it is directed that the declaration of tax liability of Rs.11,26,937/- be accepted by the Department.

18. Subject to the said amount being deposited within a period of one month, the impugned show cause notice dated 31st December, 2020 shall stand quashed. If the said amount is not deposited within one month, the impugned show cause notice dated 31st December 2020 shall automatically revive and the Petitioner is permitted to file a reply to the same. The proceedings under the impugned show cause notice would then proceed in accordance with law.

19. The petition is disposed of in these terms. All pending applications, if any, are also disposed of.